payment Basics

Article published:

A must-see for businesses. Thorough explanation of Credit card payment mechanisms, fees, contract forms, and risk countermeasures

Key points of this article

- Credit card payment Organize the roles of each company involved in the project and the flow of money and responsibilities.

- We will present the key points of the contract method, screening criteria, and cost structure that are best for your company.

- We will also explain the scope of responsibility and risk countermeasures for fraud chargeback.

INDEX

Credit cards are payment method that allow you to buy now pay later without using cash.

While the trend of cashless promotion is promoting the introduction of e-commerce sites and stores, businesses considering the introduction need to correctly understand who to contract with and where responsibility arises.

If you implement it without understanding the mechanism, you may choose a contract method that is not suitable for your company, overlook hidden fees, delays in review, and response costs in the event of a fraud.

In this article, we will explain the Credit card payment mechanism that businesses (merchants) should keep in mind, the roles and relationships of each player involved in payment (acquirers, issuers, international brands, payment processing company companies), as well as the contract method, cost structure, and risk concept.

What is a credit card?

A credit card is a buy now pay later payment method based on credit transactions that exchange payments between users, merchants, and card companies.

Specifically, payment is done in the following flow:

-

Users purchase products and services at merchants

-

The card company pays the usage fee to the merchant on behalf of the user

-

The user pays the card company at a later date

When considering the introduction of Credit card payment, it's important to first understand this basic mechanism and the fact that it is built on the "trust" that users will payment at a later date.

Credit Card Usage in Japan

In Japan, credit cards are one of the payment methods used on a daily basis.

According to statistics from the Japan Credit Association, the number of credit cards issued as of the end of March 2025 was 320.57 million.

Additionally, according to Ministry of Economy, Trade and Industry, the cashless payment ratio in 2024 is 42.8%, of which Credit card payment accounts for 82.9%.

Source: Ministry of Economy, Trade and Industry Website Created from data from the Cashless payment Ratio Calculated in 2024

With such penetration rate and high usage, Credit card payment is a top priority for businesses looking to deploy payment online.

Why can I payment with a credit card?

The reason why users can pay by credit card is because the card company has a mechanism to pay the usage fee to the member store (store). You may payment the charge from your credit card company at a later date, such as by debiting your bank account.

From the perspective of businesses, it is easier to lead to purchases even if users do not have cash on the spot or if it is difficult to payment cash in bulk due to high-value products. In addition, since there is no need to hand over cash or manage change, it is also characterized by the fact that accounting operations are more efficient.

Relationship between usage limits and margin transactions

Credit cards have a predetermined maximum amount that can be used. This maximum amount is set by the card company after checking the applicant's "annual income", "place of employment", "years of service", "employment status", "borrowing status from other companies", "whether there are any past payment delays", etc., and "whether they can continue to pay".

In addition, the limit is set individually through screening, and when the upper limit is reached, it becomes unusable until the usage balance is restored.

In this way, credit cards are credit transactions based on the premise that users can pay properly at a later date.

How Credit card payment works

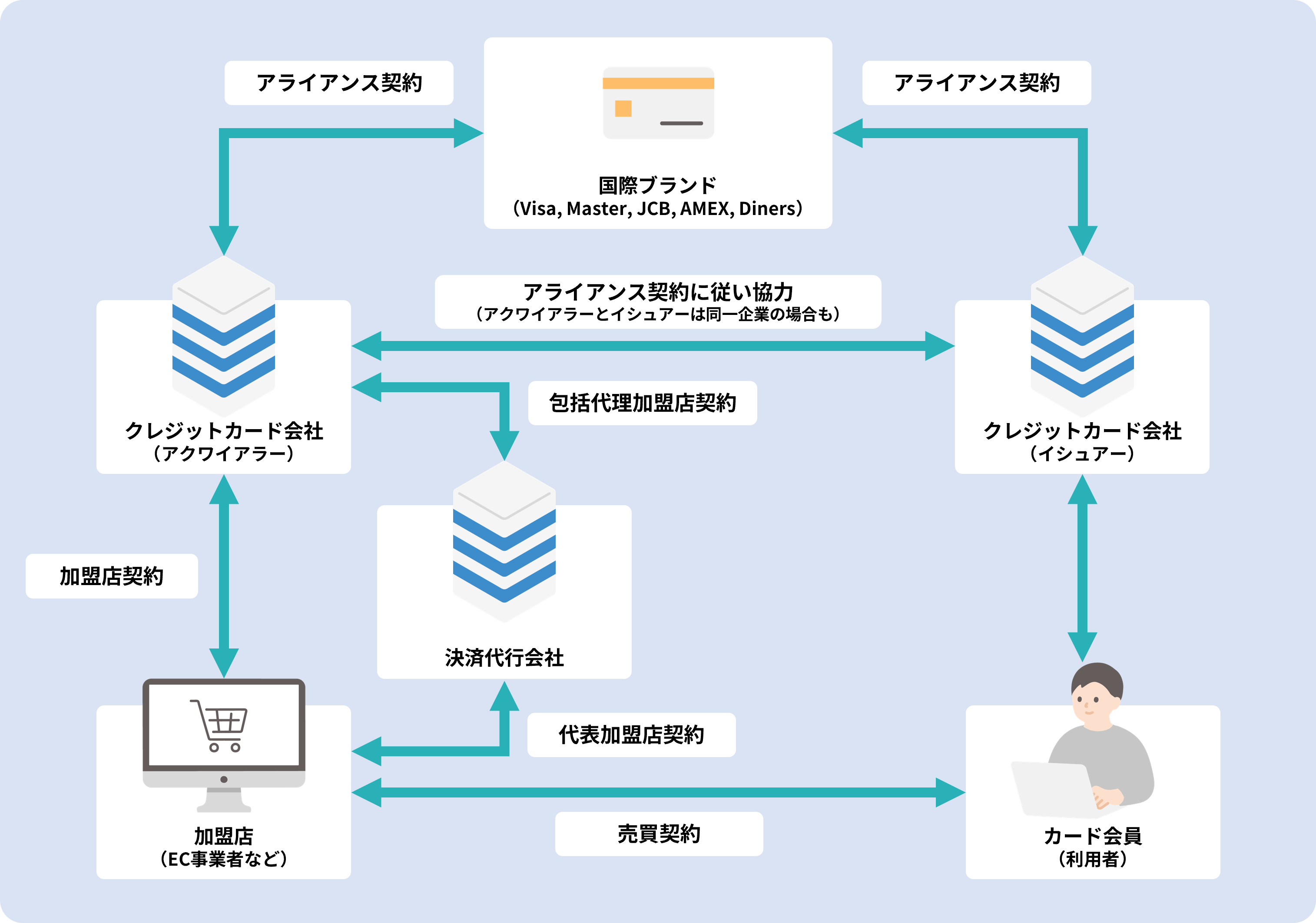

Credit card payment is a system that involves multiple positions, such as users, merchants, credit card companies, and international brands.

In order for businesses to make implementation decisions, they need to organize who plays what role and where contract and fund exchanges occur.

First, let's take a look at the basic parties in order.

1. What is an acquirer?

An acquirer is a company that develops merchants that introduce Credit card payment and manages merchant screening and contract.

When a business introduces a card payment, the direct contract method connects the acquirer with the merchant contract.

Acquirers are responsible for allowing merchants to accept cards from international brands such as Visa, Mastercard, and JCB based on their licenses and networks.

In addition to being an application counter, we are also in charge of the following practical tasks.

-

Check the products and sales methods

-

merchant screening

-

Setting Fee Conditions

-

Manage sales data

-

Deposit to merchants

-

Confirmation of operation in accordance with the merchant terms and conditions

In other words, the acquirer is "the contract destination for merchants to get started with card payment" and "the one who manages the operating rules after implementation".

Acquirers act as merchants contract companies, and are also in a position to pay merchants in exchange for sales before the payment from users is actually collected.

From the perspective of businesses, it is an existence that should be aware of as a place to receive sales.

In Korea, JCB , Sumitomo Mitsui Card, Mitsubishi UFJ Nicos , and Orient Corporation are representative examples.

You can also see that merchant screening may damage the credit of the card brand.

For example, if the product content is unclear, the refund conditions are ambiguous, or the actual operation status cannot be confirmed, the review may be strict or the contract may not be advanced.

2. What is an issuer?

An issuer is a company that recruits card members, issues credit cards, and bills and collects usage fees.

The issuer is the closest position to the cardholder (user) and is responsible for managing the usage limit, issuing invoice, debiting the account, and determining the suspension of use even after the card is issued.

When a cardholder uses a credit card, the issuer determines whether the transaction can be approved.

It's not just about whether you're exceeding your spending limit.

In general, the following points can be observed:

-

Is it within the available quota?

-

payment Is there a history of delays?

-

Isn't it an unnatural use that is very different from usual?

-

Is it considered to be used by the person himself/herself?

The Cardmember (User) will be charged for the approved transaction at a later date.

It is important to note that the issuer and the merchant (business) do not have a contract to exchange money directly in principle. Therefore, the money collected from the cardholder (user) is passed from the issuer to the acquirer, and then paid to the merchant (business).

In other words, the issuer is not only a "company that issues cards", but also "a company that temporarily takes on payment on behalf of the cardholder and collects the payment at a later date".

Major domestic issuers include Sumitomo Mitsui Card, Mitsubishi UFJ Nicos, Toyota Finance, Credit Saison, and Life Card.

JCB and American Express are international brands and also function as issuers.

3. What are international credit card brands?

International brands are payment brands that are available at merchants in Japan as well as around the world, such as Visa, Mastercard, JCB, American Express, and Diners Club.

It is easy to understand if you think of these as the ones that provide the rules and networks of the payment rather than the entity that issues the card itself.

The main roles of international brands are as follows:

-

payment Provide a network

-

Establish common rules for merchants (businesses) and card companies (acquirers, issuers) to follow

-

Grant licenses to acquirers and issuers

-

Maintain brand credibility

Generally, Visa, Mastercard, JCB, American Express, and Diners Club are the five major brands.

For businesses, which brands they support affects their purchase rates. This is because if there are few compatible brands, users may not be able to use their cards and may leave just before purchasing.

On the other hand, increasing individual contract for each brand increases the burden of contract, accounting, and sales management.

Therefore, decide how widely you want to respond according to the sales target and the operating system.

4. What is a Credit card payment merchant?

Merchants (businesses) sell and provide products and services by introducing Credit card payment on e-commerce sites, physical stores, subscription services, reservation services, etc.

(Merchants receive merchant screening through acquirers or payment processing company companies, and can use Credit card payment by connecting merchant contract.)

Once implemented, you will not only accept Credit card payment, but also have the responsibility to operate in accordance with the merchant agreement.

As a franchisee, the main points you should keep in mind in practice are as follows.

-

The products handled and sales methods will be confirmed through the examination

-

Merchant commission is charged for each sale

-

Special Commercial Law notation, terms of use, and refund conditions are required

-

You need to be prepared for fraud and chargeback

-

Member Terms of Agreement Violation payment Suspension

Merchant fees are not uniform and vary depending on the industry, sales scale, and sales method.

There may be differences in contract conditions, such as around 3% to 7% for individual businesses and 1% to 2% for national chain convenience stores and electronics retailers. It's also not uncommon for high-risk products and recurring payment-type services to be offered higher rates.

It is generally prohibited by the merchant terms and conditions for merchants (businesses) to charge users the fee for card payment as it is.

If you find a violation of the terms, it can lead to not only a request for improvement, but in the worst case, a suspension of your card payment.

Therefore, the merchant (business) is not only the "recipient of the payment", but also the "safe operation while following the established rules".

When comparing fee terms, do not judge only one company, but take a quote including the payment processing company company and compare both the total cost and the operating burden.

5. What is a cardholder (cardholder, cardholder)?

A cardholder is a person who holds a credit card and actually uses it to payment a product or service.

On e-commerce sites, you enter your card number, expiration date, Security Code, etc., and at physical stores, you payment by inserting your card, holding it up, and entering your PIN.

Cardmembers (users) do not pay cash to the merchant (business) at the time of purchasing the product, but payment the usage fee to the issuer at a later date.

From the perspective of merchants (businesses), cardholders (users) are the starting point of sales, and the ease of use of payment screens and the number of compatible brands are directly related to the purchase rate.

For example, if you are in the following conditions, you are likely to leave just before purchase.

-

I can't use my own brand of credit card

-

The identity authentication screen is difficult to understand

-

Too many fields

-

It's hard to payment on your smartphone

Therefore, merchants (businesses) need to think about designing cardholders (users) not as "mere purchasers" but as "people who will proceed to payment without hesitation".

6. What is a payment processing company company?

A payment processing company company is a company that enters between merchants, acquirers, international brands, etc., and provides contract, system connection, sales management, and payment management.

If merchants (businesses) connect individual contract for each brand, the number of application windows will increase, and it will be easier to check conditions, adjust connections, and handle accounting.

payment processing company companies are used to reduce such burdens.

payment processing company The main benefits of using a company are:

-

Easy to apply for multiple international brands at once

-

Easy to introduce non-credit card payment method at once

-

Easy to unify sales and payment management

-

refund Easy to use operational functions such as cancellation and fraud detection

-

You can organize the contact point at the time of introduction

In many cases, EC companies want to introduce not only credit cards but also CVS Payment, Account transfer, ID payment, buy now pay later, etc. In that case, it is easier to organize the implementation and operation of the payment processing company company.

It's also important to get a quote from a payment processing company company and compare terms when comparing merchant fees.

When comparing, it is necessary to check not only the high or low commission rate, but also the implementation cost and operational burden.

-

payment Commission Rates

-

Initial cost

-

Monthly cost

-

Transfer Fees

-

Types of payment method that can be supported

-

Ease of use of the admin screen

-

Support System

-

Operational functions such as fraud detection and refund processing

If you look at the items as described above, it will be easier to determine the conditions that suit your company.

The introduction of Credit card payment is detailed below.

Benefits of implementing Credit card payment for businesses

There are three main advantages for businesses to introduce credit cards:

-

Advantage 1. Easy to increase purchase opportunities

-

Advantage 2. Easy to aim for an increase in customer unit price

-

Advantage 3: Easy to reduce management burden and non-payment risk

I will explain each of them.

Advantage 1.More opportunities to buy

When Credit card payment is available, it is easier for cardholders (users) to make purchases on the spot, even if they do not have cash on hand.

For example, it is easier to prevent churn at stores because there is not enough cash, and e-commerce also makes it easier to proceed to the completion of the purchase because there is no waiting list for payment like Bank transfer.

Advantage 2.You can aim to increase the cost per customer

Credit card payment eliminates the need to have cash on hand, making it easier to reduce the psychological burden of high-value products or bulk purchases.

Even if the payment amount is likely to be large, such as home appliances, courses, and subscription-type services, if you have a Credit card payment, it will be easier to apply and purchase without preparing a lump sum of cash on the spot.

Some credit cards also allow you to choose to pay in installments, making it easier for cardholders (users) to make payment plans, which also leads to an increase in the unit price of purchases.

Advantage 3.Easy to reduce management costs and unpaid risks

At the store, it is easy to reduce the burden of preparing change, counting cash, and closing the cash register, and you do not have to put a lot of cash in terms of crime prevention.

Even in e-commerce, it is less likely to require the time and effort of confirming and reminding payments like Bank transfer, making it easier to organize the collection flow.

In addition, subscription and recurring payment make it easier to automate monthly billing, making it easier to streamline day-to-day operations.

Disadvantages of implementing Credit card payment for businesses

Next, there are three main disadvantages of businesses introducing credit cards.

-

Disadvantages 1. Installation costs and fees are charged

-

Disadvantage 2. Failure response and security measures are essential

-

Disadvantage 3: Pay attention to the deposit cycle and chargeback

I will explain each of them.

Disadvantages 1. Installation costs and fees are charged

Implementing Credit card payment may incur the purchase of payment devices, system connection fees, and monthly usage fees.

Additionally, you also incur merchant fees for each payment, so more sales may not necessarily increase profits by the same percentage.

Commission rates and fixed costs vary from company to company, so you need to compare them in total before implementing. Employee training is also a preparation item.

Disadvantage 2. Failure response and security measures are essential

If a store experiences a power outage, communication failure, or terminal failure, it may not be able to accept Credit card payment on the spot.

If a system failure occurs in EC, there is a risk that the payment screen will increase drop-offs.

You also need to be prepared for credit card breaches and fraud.

In order to operate safely, in addition to preparing a separate payment method, it is also necessary to have a system for identity authentication and fraud detection.

Disadvantage 3: Pay attention to the deposit cycle and chargeback

Credit card payment doesn't get paid immediately when sales are made.

Because there is a time lag between the closing date and the payment date, it can affect cash flow for businesses that come first in payment advertising and purchasing costs.

In addition, if you chargeback a fraud or cardholder dispute, your paid sales may be reversed. Once the item has been shipped, you will be left with a loss.

Credit card payment contract Pattern

The contract of Credit card payment can be broadly divided into two types: the "direct contract method" and the "inclusive merchant method". First of all, it is easier to determine the method that suits your company if you organize the overall differences in a table.

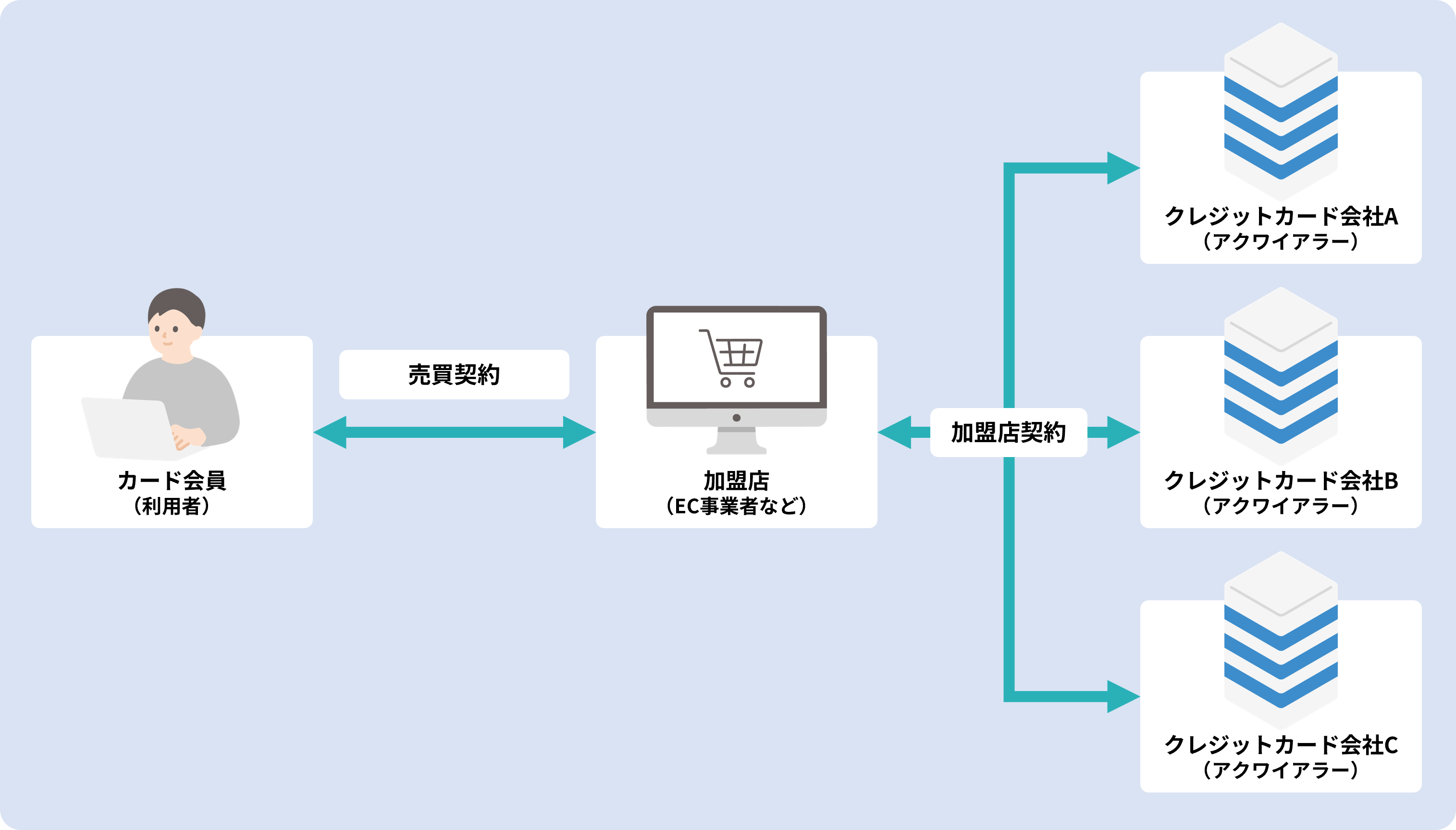

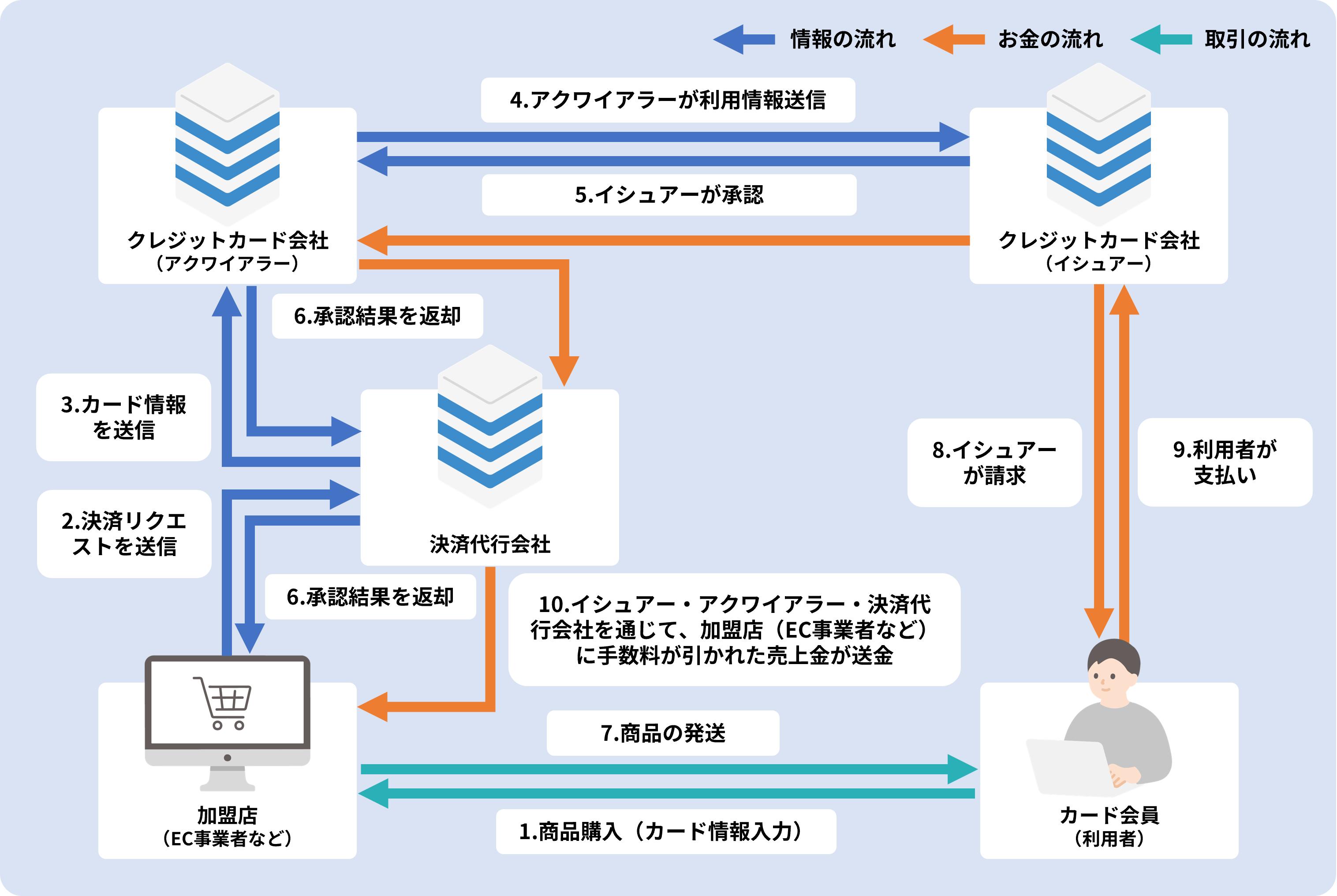

How the Direct contract Method (Four-Party payment) Works

The direct contract method is a contract form consisting of four parties: cardholders (users), merchants (businesses), acquirers, and issuers.

In order for merchants (businesses) to introduce Credit card payment, they must first connect the acquirer with the merchant contract and pass the screening of the products handled, Business Overview, site notation, etc.

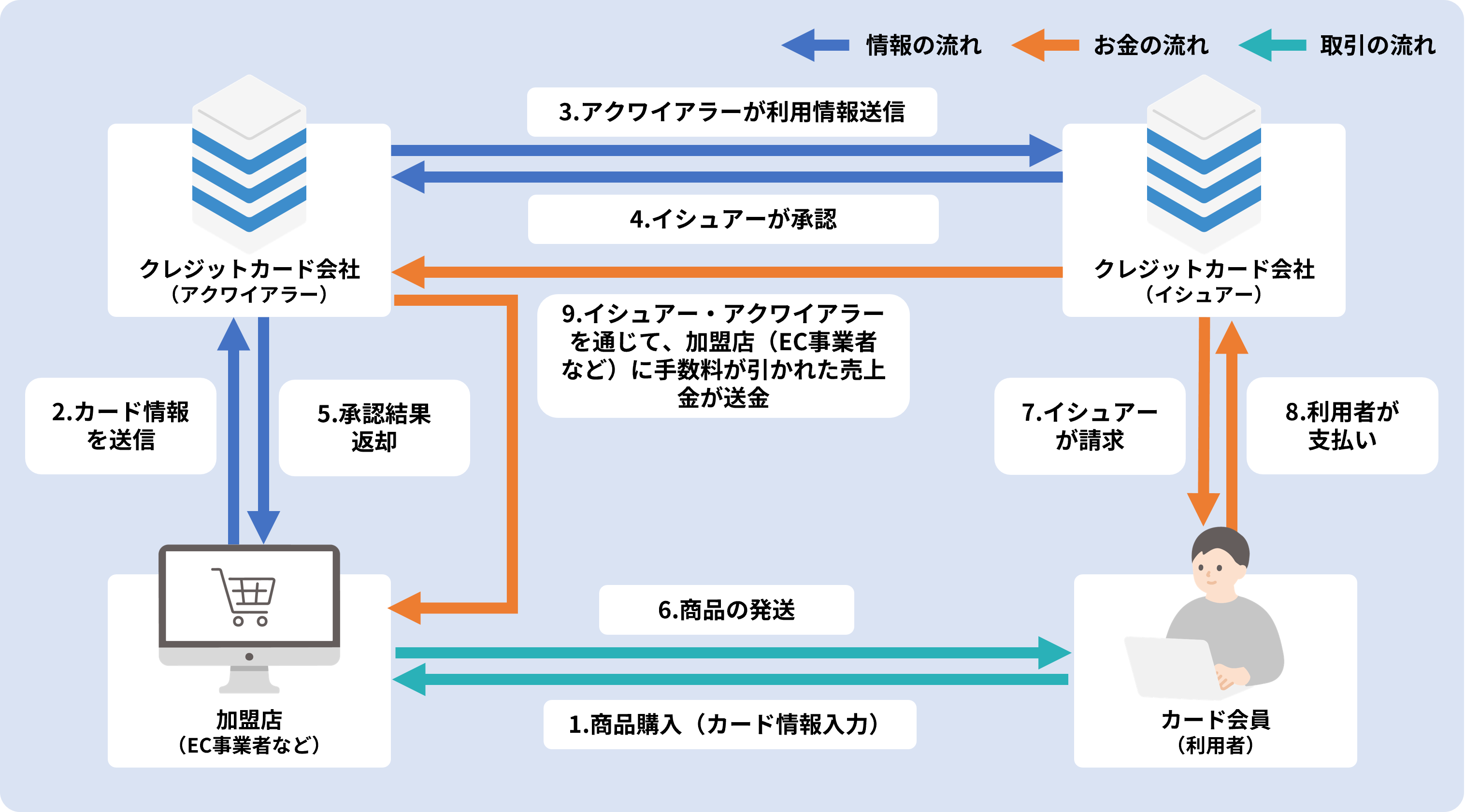

payment, the Cardmember (User) purchases the product and the usage information is sent to the issuer via the acquirer.

Once approved, the sale is concluded, and the merchant (business) proceeds to ship the product and provide the service.

After that, the issuer charges the card member (user) for the usage.

Cardmembers (users) make payment by Account transfer and other methods, and the issuer payment the repaid sales proceeds to the acquirer.

In addition, the acquirer credits the merchant (business) with the proceeds, where the prescribed payment fee is deducted. From the point of view of merchants (businesses), it is necessary to understand that cash is not immediately converted at the point of sale, but is deposited at a later date depending on the closing date and payment date.

The characteristic of the direct contract method is that merchants (businesses) contract individually with the acquirer to adjust conditions and design operations.

On the other hand, if you want to support multiple brands, such as Visa, Mastercard, or JCB, you may need to contract and confirm with the acquirer with their respective licenses.

As a result, not only will the application process increase, but the screening conditions, merchant terms, connection specifications, payment cycles, and accounting processing rules may vary from contract to destination, making it easy to increase the burden both at the time of introduction and after the start of operation.

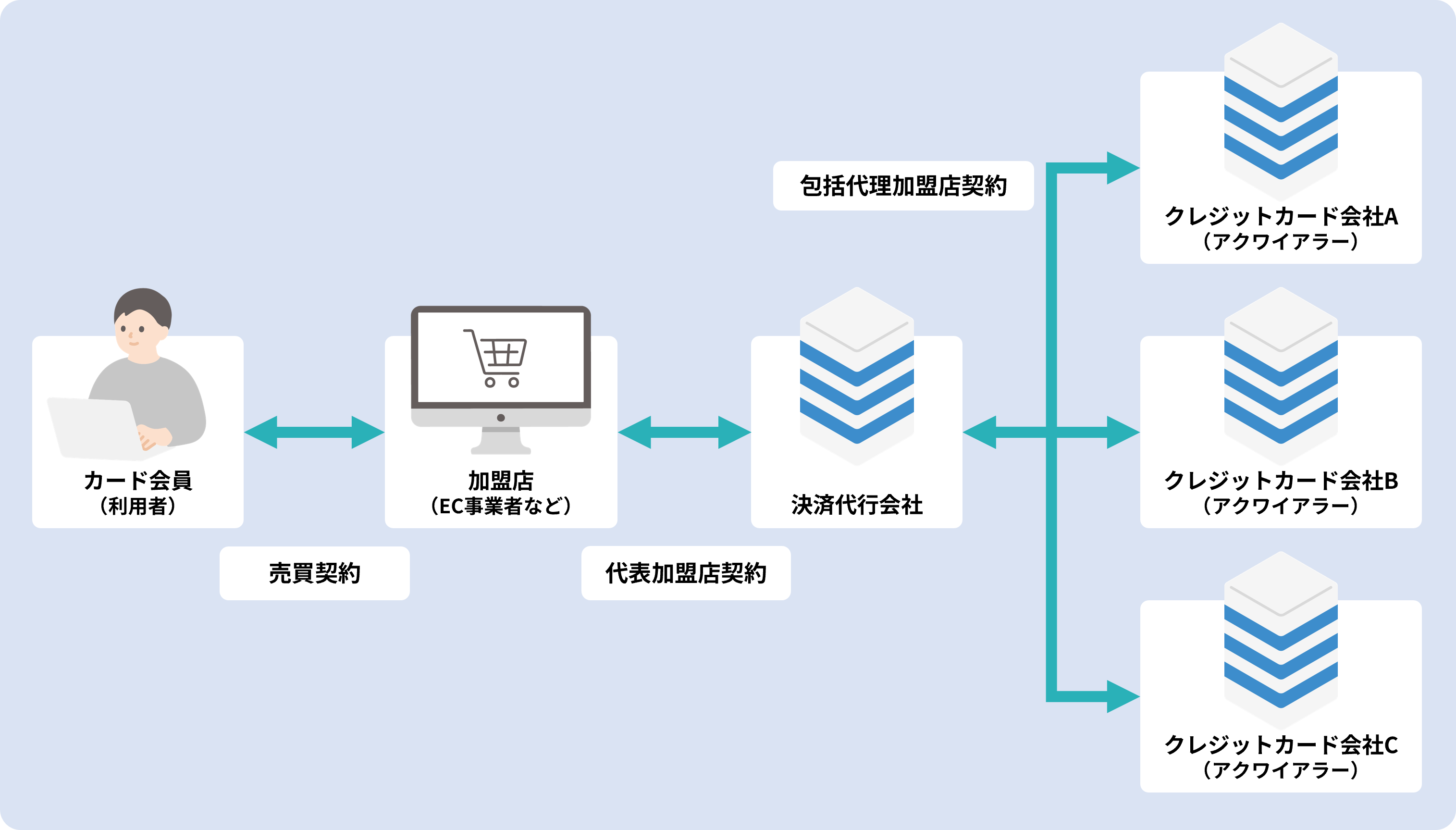

Mechanism of the comprehensive merchant system (payment processing company 5 parties including the company payment)

The inclusive merchant method is a five-party contract form in which payment processing company companies join the four-party flow.

The following table explains the differences between them.

|

Compare items |

Direct contract (4-way payment) |

Including franchise store method (5 parties payment) |

|

contract ahead |

Operators and acquirers directly contract |

Businesses and payment processing company companies contract |

|

Involved |

Cardmembers, merchants, acquirers, and issuers |

Cardholders, merchants, payment processing company companies, acquirers, and issuers |

|

Effort at the time of introduction |

Brand contract and adjustments are likely to be required |

Easy to organize the application window |

|

Operational burden |

Easy to decentralize deposit conditions and contract management |

Easy to consolidate management |

|

Suitable cases |

If you want to adjust the contract conditions individually |

If you want to reduce the burden of introduction and operation |

The difference is who the merchant (business) contract with, the time and effort at the time of implementation, and how to manage payments and operations.

In the preliminary preparation, the merchant (business) enters into a contract with the payment processing company company and applies for the desired brand and payment conditions together.

In payment case, the usage information of the cardholder (user) will be linked to the acquirer and issuer through the payment processing company company's system, and the sale will be completed after approval.

In terms of deposits, the payment processing company company consolidates payment to merchants (businesses), making it easy to unify the operation of multiple brands.

contract It is suitable for businesses that want to consolidate contact points and management, and it is easy to reduce the burden of introduction.

Judged by the growth phase of the business and the operation system! contract Selection criteria for the method

Credit card payment 's contract approach should be chosen based on the size and operational structure of the business, as well as its future scalability. Here, let's sort out which method is easier to choose at which growth stage.

If you want to focus on your main business and optimize management costs, you can use the "comprehensive agency franchise method"

The most reasonable method at the start-up stage of a business or the start of a new business is the comprehensive agency franchise method.

In this method, the payment processing company company acts as a point of contact with multiple payment services, including the acquirer, so that the business can unify the procedures related to contract, screening, system connection, and sales receipt.

In particular, the new business phase requires more resources to be devoted to non-payment tasks, such as product development, sales preparation, and customer attraction preparation. In this context, if you contract and negotiate with multiple card companies individually, and handle payment management and inquiry response separately, it will be difficult to concentrate on core operations, and there is a risk that management costs will be heavy.

The biggest advantage of choosing the comprehensive agency method is that you can leave the complicated parts of payment to the expert payment processing company company and focus on the growth of your main business.

Individual negotiations are possible, but the "direct contract method" requires attention to the overall cost

The direct contract method is a format in which the acquirer and the contract are individually connected.

The biggest advantage of this method is that it allows you to negotiate the terms and conditions of the commission rate and the operational design in detail with specific card brands and acquirers. Large, mature businesses with a large monthly payment volume or a desire to focus on a specific brand may consider it.

However, it should be noted that this is not a comparison in terms of commission rates, but a multifaceted comparison when viewed in terms of overall cost.

In the direct contract method, contract for each destination:

-

Application, screening, condition negotiation, system connection required

-

Sales confirmation, payout management, refund processing, and inquiry response all need to be done separately

-

In-house compliance with PCI DSS and other security standards, and the associated significant development and operation costs

It is necessary to deal with the cost. If it is not possible to secure a dedicated person in charge or if it is difficult to secure resources for security response, the total cost will be higher than using the comprehensive agency method and there is a risk of increasing the operational burden.

What to see in merchant screening and why you fail the review

Credit card payment is not available immediately after you sign up.

merchant screening mainly see the following four points.

-

Product Contents

-

Business Reality

-

Sales site display

-

Historical Transaction Status

Any uncertainties or concerns about any of them can lead to prolonged review or unapproval.

The products handled do not meet the screening criteria

The first thing that is easy to see is the content of the product that sells what it sells.

Credit card payment not all products are treated to the same standards, and products that are likely to be considered risky are carefully reviewed.

For example, recurring payment-type services, high-priced products, or products with unclear delivery dates may be seen as prone to refund and trouble.

If the product description is ambiguous, it will be difficult for the judge to judge the actual situation.

It's essential to be clear about what and how you're going to deliver it.

Unable to confirm the actual business status (company information and management system)

If the company information and management system are not clear, it is easy to be at a disadvantage in the examination.

The reason is that since you are dealing with payment, you need to check whether the business can continue to operate.

If the company name, location, contact information, and representative information are missing, or if the contact information is not functioning, it will be difficult to see the actual situation of the business.

Uncertainty about who will handle refund and customer interactions can also lead to operational anxiety.

The basic information and management system of the business are items that should be sorted out before the examination.

Incomplete notation on the sales site (lack of notation under the Special Commercial Act and terms of use)

As an item that is strictly confirmed, there is a mandatory item of "notation based on the Specified Commercial Transactions Act".

-

Selling price (handling of shipping costs and consumption tax)

-

When and how to payment the price

-

Delivery time of the product (specific description such as "within ○ days after completion of payment")

-

Special Contract for Returns, Exchanges, and Cancellations (even if it is "non-returnable", it must be stated to that effect)

If these are insufficient, it will be difficult to see the response policy in case of trouble with users, and it will be difficult for the reviewer to judge the risk.

In particular, in the case of "subscription", the cancellation conditions and total price display have become stricter due to legal revisions, so be sure to review whether these are properly covered before publishing the site.

Reference: Revision of the Specified Commercial Transactions Act and the Depository Act in Reiwa 3

There is a problem with past transactions and credit information

The past payment management Actual and credit aspects of businesses applying as merchants may also be seen in the examination.

For example, if there were many payment problems in the past, "chargeback was frequent", or "there was a problem with a contract company", it is easy to make a careful decision.

In addition, if it is deemed that there is concern about business continuity or payment ability based on financial statements in the case of corporations and data from designated credit information agencies (CIC, etc.) in the case of sole proprietorships, it may affect the screening.

If you don't have a Actual for a new business, you will often be asked to provide the representative's background and business plan documents.

payment Fee Structure and Fee Structure

Don't judge the cost of Credit card payment based solely on apparent commission rates.

In practice, in addition to the breakdown of payment fees, the burden may vary depending on the contract methods of "direct contract" or "general distributor method".

Organize the structure of fixed costs and variable costs so that you don't end up spending more than expected after implementation.

payment Fee Breakdown

payment The fee is not a single cost, but consists of three main components:

-

Interchange fee: cost to the card issuer (issuer)

-

Brand network fee: Visa/Mastercard usage fee

-

Acquirer revenue: Operating Expenses and Profits of Merchant Management Company

The sum of these is the Merchant Discount Rate.

In recent years, there has been a growing transparency in Japan, such as the disclosure of the standard rate of interchange fees, and it is important to check whether the rate presented is based on a reasonable "purchase price".

Differences in rates depending on industry type and sales scale

payment Commission rates are not uniform and are estimated based on the industry, product characteristics, chargeback susceptibility, and monthly payment throughput.

Ministry of Economy, Trade and Industry also indicates that merchant fees are determined by negotiations between merchants and acquirers, and that publishing the standard interchange fee rate will make it easier to negotiate prices.

For example, recurring payment-type services and high-value products are likely to be viewed with caution due to refund and fraud risks, which can affect rates.

On the other hand, businesses with large monthly payment handling volume and stable sales are more likely to adjust merchant commission rates and payment conditions individually because they are expected to have continuous transactions.

Reference: Ministry of Economy, Trade and Industry | Summary of the Cashless Promotion Study Group (draft)

International payment multi-currency payment and Currency Risk Considerations

As e-commerce businesses become increasingly globalized, catering to multi-currency payment becomes essential when targeting international customers.

When implementing multi-currency payment, you should be aware of the following cost items and risks:

- Exchange fees: These are fees set by international brands and payment processing company companies when converting currencies.

- Exchange rate risk: This is the risk that the profits of merchants (businesses) will fluctuate due to fluctuations in the exchange rate between the time the sales are confirmed and the payment is received.

payment processing company Some companies may provide a "foreign exchange risk bearing service" that guarantees payment in Japanese yen at the exchange rate at the time of confirmation of sales. When considering overseas expansion, not only low commission rates, but also such a support system for foreign exchange risk management are important factors to consider.

Cost Difference between Direct contract and General Distributor Methods

The direct contract and general distributor methods look different in terms of costs.

-

Direct contract: While rates are easy to keep low due to the lack of intermediate margins, the operational burden can be high, including different payout management for each brand and PCI DSS (an international security standard for protecting the environment in which card information is stored, processed, and transmitted). In particular, PCI DSS requirements are stringent and require significant costs (capital investment, professional talent acquisition, audit costs) to comply and maintain on your own.

-

Comprehensive Affiliate Method: The advantage is that it is easy to integrate contract, system connection, and sales management, and it is easy to introduce multiple payment method at once. On the other hand, it can be more expensive compared to the direct contract method.

Cost comparison should be judged not by the "point" of the rate, but by the total cost of ownership, including the labor cost of the back office.

Cost items to check when estimating

When reviewing estimates, don't judge by payment commission rates alone.

contract The burden is likely to increase later in cases where overlooked expenses come out later.

When estimating, it is easier to make a decision if you check the following items together.

-

payment Commission Rates

-

Initial cost

-

Monthly cost

-

Transfer Fees

-

refund and cancellation fees

-

Additional cost for optional features

If you organize these expenses first, it will be easier to reduce the risk of realizing that the cost is different from what you expected after contract. Be clear about how much it will cost as a total amount.

Impact on Deposit Cycles and Cash Flow

Credit card payment doesn't immediately credit your account when a sale occurs.

Depending on the setting of the closing date and payment date, there is a time lag before it is actually funded.

To avoid financial difficulties after implementation, you need to check the deposit mechanism before contract.

How payment timing (closing date and payment date) works

In Credit card payment, the sales date and the payout date are not the same.

The timing of payment is determined by when sales are counted and when they are transferred.

In general, there are many settings such as "closing twice a month, 15th buy now pay later" or "closing at the end of the month, paying at the end of the next month", and there is a range of about 15 to 60 days from sales to payment.

Understanding the combination of closing and paying dates can help you see when your funds will move.

Period from sales confirmation to receipt

There is a certain period of time between when the sales are confirmed and when the money is deposited.

Even if the cardholder's (user's) payment is approved, the funds will not be immediately credited to the merchant (business), but will go through the steps of sending "sales billing data", processing settlement at the card company, and executing the transfer.

If this "unpaid period" is long, there is a risk that the business model will run the payment of advertising and purchasing expenses ahead of the cash on hand.

If you're dealing with high-priced or seasonal products, it's essential to consider this period.

Points to prevent cash flow from deteriorating

To prevent cash flow from deteriorating, it is important to look not only at the amount of sales, but also at the speed of payment.

Even if the commission rate seems low, if the number of days until deposit is long, it is easy to run out of funds on hand.

In particular, during the business start-up period and the period of strengthening sales promotion, it is easier to spend first. It is necessary to check the deposit conditions, transfer fees, and expected payment dates, and have a reasonable financial plan.

Risk management to prepare for fraud and chargeback

Credit card payment requires not only a design to increase sales, but also a perspective that prepares you for fraud and chargeback.

According to the Japan Credit Association, the amount of credit card fraud damage in 2024 was 55.50 billion yen.

Since there is no face-to-face confirmation in e-commerce and online payment, it is necessary to organize the scope of responsibility and countermeasures from the time of implementation.

Reference: Japan Credit Association|Credit Card fraud 5 Measures

fraud The basic responsibility at the time of the event occurs to the merchant (business)

In EC, there are situations where it is necessary for merchants (businesses) to confirm and respond when fraud occurs.

Therefore, it is necessary to have an operation in place to check large orders, continuous orders in a short period of time, and orders with very different billing and shipping destinations separately from regular orders.

Individual verification here is to check the customer's name, phone number, email address, shipping address, past purchase history, and order content for any unnatural points.

If you are purchasing multiple high-value items even though it is your first purchase, it is helpful to be able to review the order details before shipping to prevent fraudulent delivery.

It is easier to reduce damage if you do not ship only the system's judgment results and have a flow that allows people to check orders that meet certain conditions.

chargeback Sales are canceled when they occur

When a chargeback occurs, in addition to canceling sales, you will also need to submit confirmation documents and take internal action.

chargeback is a system in which a cardholder (user) complains to the credit card company that "this use is not his" or "the product has not been received", and as a result of the investigation, the card company cancels the payment.

For merchants (businesses), the burden is high because the recorded sales are canceled at a later date, and they are required to respond to refund and submit explanatory materials as needed.

If the appeal is granted, sales may be restored, but you need to be able to provide evidence of the transaction.

Therefore, keep the date and time of your order, the products you purchased, user information, shipping records, inquiry history, and your agreement to the terms of use.

If it is a digital product, it is easier to explain the actual transaction situation by keeping a record of when you logged in with the account you purchased, when you started using it, and when you downloaded or watched it.

chargeback Specific flow of Protest and points to increase the winning rate

Please note that even if an chargeback occurs, merchants still have the right to "appeal". Not all sales are canceled at the time of finalization.

Appealing is the process of submitting documents to prove that the transaction is legitimate in response to a chargeback notice sent by your card company. To increase your chances of winning, it's essential to have materials that cover the following points:

1. Data at the time of order and contract: date and time of order, IP address, device used, and record of acceptance of the terms and conditions.

2. Proof of product shipment and delivery: carrier tracking number (proof of completion of delivery), and in the case of digital content, usage logs and download records.

3. Communication history with users: Records of emails after ordering, inquiries, and explanations of refund policies.

Responding to this objection requires time and expertise, so accurately storing daily transaction records and working with payment processing company companies to create a system that allows for rapid response is the "last bastion" of chargeback measures.

The introduction of identity authentication (3D Secure) changes the scope of responsibility

3D Secure 2.0 (EMV 3-D Secure) is a mechanism that checks the identity of the cardholder at Credit card payment time.

By implementing it, merchants can reduce the risk of losing money when a fraud occurs.

The current 3D Secure does not uniformly require additional authentication for all orders.

It is common to determine risk based on information such as order amount, purchase history, delivery destination, and device used, and perform additional authentication only for transactions that are deemed necessary.

For example, if you're ordering a high-value item despite your first purchase, if you're making multiple payment in a short period of time, or if your billing and shipping destinations are very different, it's easier to be scrutinized.

Fraud detection services can reduce risk

Since e-commerce cannot verify your identity face-to-face, you cannot judge fraudulent orders based solely on appearance.

On the other hand, the more orders you have, the more difficult it is to see all transactions with the human eye alone. This is where the "fraud detection service" is used, which automatically finds orders suspected of fraud.

In order to effectively use fraud detection services, it is important to first decide what orders are considered dangerous by your company.

For example, short-term continuous payment, large orders from overseas IPs, use of multiple cards on the same device, and unnatural combinations of names and email addresses are easy to set as verification targets.

If these standards remain ambiguous, the accuracy of detection and operational decisions can easily be shaken.

It is also necessary to organize the response after detection in advance. If you decide whether to automatically reject orders that are judged to be high-risk, turn them to visual verification, or add identity verification, you will be able to respond to the scene stably.

Combining 3D Secure with fraud detection services makes it easier to prepare for fraud in terms of identity verification and anomaly detection.

Conclusion

Let's summarize the overall points explained so far in the following table.

|

Points of concern |

Conclusion |

Checkpoints required |

|

What are the multiple stakeholders involved in Credit card payment and their roles? |

Credit card payment consists of multiple stakeholders (e.g., issuers, acquirers, payment processing company companies, etc.). |

Acquirers, Issuers, International Brands, payment processing company Company Roles and Where Money and Responsibilities Reside. |

|

How to choose the contract method (direct contract method/inclusive merchant method) that suits your company? |

Depending on the business scale and operational system, the most suitable contract method should be selected. |

Advantages and disadvantages of the direct contract method and the comprehensive agency method respectively. |

|

What does Credit card payment merchant screening check? |

Screening is conducted from multiple perspectives, such as product content, business conditions, and sales site notation. |

Are there any deficiencies in the products handled, the actual state of the business, the notation of the Special Commercial Law, and the terms of use? |

|

payment What is the cost structure of the fee other than the rate? |

Fees should be determined by the total cost of ownership, including rates, fixed costs, and operational burdens. |

payment Expense items that should be checked in total, such as commission rate, initial cost, monthly cost, transfer fee, refund cancellation fee, etc. |

|

What are the points to check for correct understanding of the deposit cycle and cash flow? |

It is necessary to correctly understand the deposit cycle and make a reasonable financial plan to avoid depleting cash on hand. |

The timing of the closing date and payment date, and the period from sales confirmation to payment. |

|

What is the scope of responsibility and risk management in the event of a fraud chargeback? |

Fraud countermeasures are essential, and risks can be reduced by combining identity authentication and fraud detection. |

Change the scope of responsibility due to the introduction of identity authentication (3D Secure), use of fraud detection services, chargeback response flow when it occurs. |

|

How to make a smooth Credit card payment decision? |

payment Recognize that professional confirmation is necessary for design, and consider consulting with payment processing company companies with specialized knowledge. |

payment Whether or not there is a consultation desk and support system where you can check the design together. |

What businesses should look at is not only "which company is involved".

Only by organizing how to proceed with contract, ease of screening, cost, payment conditions, and fraud measures will it be easier to make an introduction decision that suits your company.

If you are unsure about how to introduce a Credit card payment or the design of a payment that suits your company, please feel free to contact our sales for any small consultation, such as "I am worried about whether I will pass the examination" or "I want to know the market price of the cost". We will propose the optimal payment design according to your company's business phase and product products, after organizing the points necessary for the introduction decision.

Service Introduction

PG Multi-Payment Service

PG Multi-Payment Service is a payment platform provided by GMO Payment Gateway, Inc., a payment processing company company (PSP, Payment Service Provider). It has been introduced to a wide range of businesses, from startups to small ~ large companies, regardless of industry or size.

It provides a solid infrastructure to support a huge payment of 163,890 stores, an annual Transaction value of 21 trillion yen, and 7.22 billion cases processed (*). In addition, it is fully compliant with the global security standard PCI DSS Ver4.0.1, helping any business to create a secure payment environment.

- Supports payment and subscriptions (subscription and recurring payment) each time

- Connection methods are available to suit your needs (OpenAPI type, Link type Plus)

- HDI International Certified Customer Support Department Gate Provides Generous Support

*As of the end of September 2025, consolidated figures

![]()

Author

PX+ by GMO Editorial Department

The PX+ by GMO editorial team is a dedicated media team specializing in the payment and Payment Experience (PX, payment experience) area by GMO Payment Gateway.

payment ・Based on the latest trends and practical know-how related to e-commerce operations and cashless in general, as well as examples of growing companies, we compile and supervise practical and reliable information that is useful for business growth.

Click here for the purpose of "PX+ by GMO" and the list of supervisors.